Africa’s trade finance gap could widen to $86.6bn as Middle East tensions linger

The African Development Bank (AfDB) has warned that Africa’s trade finance gap could widen to $86.6 billion by 2027, with rising geopolitical tensions in the Middle East increasing energy prices and tightening global credit.

The report, Trade Finance Supply in Africa: Post-COVID Trends and Emerging Opportunities, estimates that Africa’s unmet demand for trade finance in Africa ranged from $74 billion to $92 billion in 2024. The estimated gap of $74 billion represents 5.4 percent of the region’s total merchandise trade value in 2024.

“This outcome was underpinned by swift and substantial interventions following the COVID-19 pandemic from multilateral development banks, governments, export credit agencies, and others,” the report said.

Anthony Simpasa, Director of the Macroeconomic Policy, Forecasting and Research Department at the African Development Bank, said unmet demand for trade finance declined by nearly 10 percent between 2019 and 2024, supported by strong interventions from multilateral development banks, governments, export credit agencies, and global banks.

These interventions were critical in sustaining trade flows, with estimates suggesting that, in the absence of DFI support, the annual trade finance gap could have exceeded $100 billion during the 2020-2024 period.

“Renewed geopolitical tensions and disruptions to global supply chains and trade flows could reverse post-pandemic progress in narrowing the trade finance gap. For instance, a tighter correspondent risk appetite could widen the trade finance gap to $86.6 billion -$102.6 billion by 2027 under a moderate to severe scenario. This is at least 17.7 percent above the 2024 level, potentially erasing a decade of gains,” Simpasa cautioned.

The COVID shock and its aftermath

The scale of the COVID-19 disruption to African trade finance was severe. Bank-intermediated trade finance collapsed by approximately 52 percent in 2020, falling to an estimated $195 billion from $408 billion the prior year. The recovery that followed was real but incomplete. By 2024, the figure had risen to $335 billion, still more than 17 percent below the pre-pandemic level.

The proportion of total African trade supported by bank intermediation tells a similar story of structural retreat. Banks intermediated an average of just 23 percent of Africa’s merchandise trade between 2020 and 2024, compared to 40 percent in the 2011–19 period. By comparison, approximately 80 percent of global trade is supported by bank trade financing.

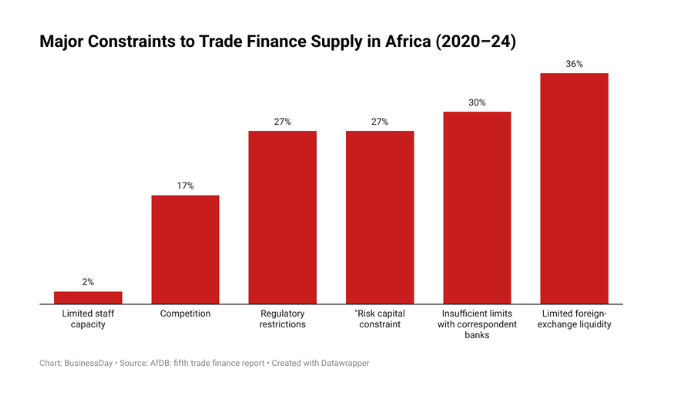

The report disclosed that foreign-exchange liquidity emerged as the dominant constraint, cited by 36 percent of banks, double the 18 percent who identified it as the main barrier in the 2015–19 period.

The US dollar continues to dominate, accounting for 88 percent of foreign exchange volumes traded. When the pandemic cut off tourism and export earnings in hard currency, banks and traders alike were caught short. Capital outflows compounded the problem, weakening local currencies and pushing African institutions toward local-currency solutions that remain, in many cases, underdeveloped.

Small businesses bear the brunt

Nowhere is the access problem sharper than for small and medium-sized enterprises (SMEs), which account for at least 80 percent of businesses across Africa and more than half of GDP. Banks approved only 63 percent of SME trade finance applications on average over the study period, compared to an overall approval rate of 80 percent. SME default rates on trade finance, while higher than those for larger clients — ranging from 8 to 9.9 percent during the period remained stable and more predictable, suggesting opportunity rather than prohibitive risk.

“Given the importance of African SMEs in driving socioeconomic fundamentals, such as employment and economic growth, addressing the acute lack of access to trade finance across the continent would consolidate the sector’s strategic importance,” the report stated.

The two most-cited reasons for rejecting trade finance applications, including weak client creditworthiness (48 percent of banks) and insufficient collateral (39 percent), have remained unchanged since the AfDB’s inaugural trade finance report in 2014.

Compliance burdens tied to know-your-customer and anti-money-laundering regulations were cited by 20 percent of banks, while limited foreign-exchange liquidity was cited by 19 percent.

Francisca Tatchouop Belobe, Commissioner for Economic Development, Trade, Tourism, and Industry, called for eliminating the ‘missing middle’ in African banking.

“SMEs are too large for microfinance, too small for corporate banking, but far too commercially important to be left outside the trade finance system. It is time for commercial banks to treat SME trade finance as a deliberate, core business line, not a residual activity,” he said.

A Shifting Correspondent-Banking Map

One of the more striking shifts revealed by the survey is in the landscape of correspondent banking. In preceding surveys, only two African banks featured in the top 10, confirming banks for African issuing institutions.

In the survey covering 2020–24, six of the top seven confirming banks are African, led by UBAF, Banque Centrale Populaire, Absa, Crown, EBI, and BMCE. Citibank retains the top position overall, with confirmation relationships with 11 percent of African banks surveyed.

The rise of regional African institutions as correspondent banks reflects both the retreat of European banks under tightening regulatory requirements and the growing capacity of homegrown institutions — supported in part by DFI programmes such as the AfDB’s own risk-participation agreements, which have supported 3,100 transactions worth $8.8 billion in total trade since the programme’s inception.

The report dedicates significant space to digitalisation, which it frames as both an opportunity and a gap. Only 28 percent of surveyed banks report having adopted digital tools or platforms for trade finance operations, well behind the 42 percent figure for the Asia-Pacific region in 2024.

Yet those that have digitalised report meaningful returns: 56 percent recorded significant improvements in operational efficiency, and 47 percent saw improvements in client satisfaction. Banks that make a full transition to digital trade finance expect to cut transaction costs by more than 30 percent, according to 35 percent of respondents. The main barriers are high implementation costs (cited by 49 percent) and inadequate technological infrastructure (28 percent).

Mauritius became in 2025 the first African country to adopt the UN Model Law on Electronic Transferable Records, which enables fully electronic trade finance instruments.

The Strait of Hormuz risk

The most urgent section of the report concerns what the authors describe as a fresh and potentially severe headwind. The outbreak of conflict in the Middle East in February 2026 and the resulting closure of the Strait of Hormuz, through which roughly one-fifth of global oil supply transits, has driven sharp increases in energy and freight costs that translate directly into higher import bills, currency pressures, and tightening fiscal space for Africa’s predominantly net oil-importing economies.

At least 29 African currencies have depreciated since the conflict began. Higher import costs are eroding the creditworthiness of African borrowers in the eyes of international correspondent banks, compressing the supply of trade finance precisely as demand intensifies.

The report models three scenarios for how the gap might evolve by 2027. In a baseline scenario with no exogenous shock, the gap continues to narrow toward $65 billion. Under a moderate scenario, sustained oil prices above $105 per barrel and tighter bank risk appetite, the gap rises to approximately $86.6 billion by 2027, a 17.7 percent increase from 2024.

In a severe scenario involving prolonged Strait of Hormuz disruption, sharp currency depreciation, and contraction in international trade credit lines, the gap reaches $102.6 billion, effectively returning to 2017 levels and erasing a decade of progress.

“Without a coordinated response from commercial banks, export credit agencies, and development finance institutions comparable to the pandemic-era financial injections, the trade finance gap risks climbing back toward, or beyond, its prepandemic average,” the report added.

Comments are closed.